The Microeconomic Consequences of Macroeconomic Performance

August

8, 2002 "Don't Cry For Me Argentina" (from Andrew Lloyd

Webber's

Evita)

was a big hit song around the world in the late 1970s. This year

the world is lamenting Argentina's economic woes. The

country

is currently on course to set a record for the largest number of people

to lose the most wealth in the shortest period of time. Argentina

is surely an economy to cry for.

August

8, 2002 "Don't Cry For Me Argentina" (from Andrew Lloyd

Webber's

Evita)

was a big hit song around the world in the late 1970s. This year

the world is lamenting Argentina's economic woes. The

country

is currently on course to set a record for the largest number of people

to lose the most wealth in the shortest period of time. Argentina

is surely an economy to cry for.

Unemployment in Argentina has climbed to 25%. The real GDP is projected to decline this year by approximately 10-15%, the largest single-year decline on record and following three consecutive years of recession that began in 1999. After nearly a decade of relatively stable prices, inflation is currently in triple digits. In April the IMF tentatively estimated that prices would increase by 30% or more this year. However, month-to-month prices jumped by 10% in April alone. If prices were to continue to escalate at that monthly rate for twelve consecutive months, then the annual rate of inflation would exceed 200%! Currency markets have already factored in April's inflation rate, and the floating peso has fallen to about $0.27 from the 1 peso = 1 dollar parity that Argentina managed to fix throughout most of the 1990s. Argentina's MERVAL stock market index has declined by nearly 75% since the end of last year. Measures of macroeconomic activity for a semi-industrialised economy rich in natural and human resources don't get much worse than these.

Like the Great Depression of the 1930s, the stagflation of the

1970s,

and the economic implosion of the former Soviet Union in the 1990s,

Argentina's

economic collapse should remind us all of how fragile economic systems

really are and how important it is to have sound economic institutions

in place and effectual corrective policy on stand-by when things start

to go wrong. The consequences of a dire economic performance have

devastating and long lasting negative psychological effects on those

persons

who suffer and endure the hard times. Individual confidence is

shattered,

and hope is overwhelmed by despair. Fear and uncertainty paralyze

the economy. Practical solutions get lost in a deluge of

ideological

polemic while the economy continues to flounder. Years, if not

decades,

of economic stagnation can pass by before confidence, stability and

growth

are eventually restored. This, it would appear, is Argentina's

fate.

Going From Good, To Bad, To Ugly

After initiating a series of free-market economic reforms in 1991, Argentina's cyclical macroeconomic performance could fairly be rated as "very good" or even "almost perfect." The economy appeared to be responding favorably to more open trade, privatization, and the implementation of a currency board to officially fix the peso to US dollar exchange rate at a 1/1 parity. The average annual rate of growth for Argentina's economy from 1994 to 1998 was just over 4%. Annual inflation averaged a mere 1.84% over that same time period. To be sure, Argentina continued to have structural unemployment and poverty problems; however, the overall macroeconomic performance was better than most other economies in Latin America and the rest of the world.

It was in 1999 that Argentina's economy turned "bad." Real GDP fell by 3.4%. Unemployment began to rise. Stock prices began to fall. Hopes for a quick recovery were dashed when the economy declined by nearly 1% again in 2000. The year 2001 was even worse when the economy recorded another 3.7% decline in real GDP. By this time, Argentina had become bogged down in an "L" shaped recession. There are several explanations for Argentina's downward slide. Most explanations focus on a series of adverse external shocks including a decline in international commodity prices, the rising cost of of capital for emerging market economies, the Brazilian real devaluation, an overvalued peso pegged to an appreciating US dollar, and higher interest rates caused by a restrictive monetary policy in the United States. Argentina's currency board system and commitment to a fixed exchange rate made it virtually impossible for monetary authorities to respond to these shocks.

This year's economic events in Argentina have turned downright "ugly." The economy is rapidly racing to severe stagflation. The first quarter recorded a 16% (average annual rate) decline in real GDP. Investment spending plummeted 46% and personal consumption expenditures dropped 21% from a year earlier. Unemployment continues to rise. Inflation is escalating rapidly from double to triple digit. After the government squandered its official reserve assets to support the peso, the floating peso is in a free fall. The government has defaulted on its external debt obligations. Businesses and banks are failing. Bank assets have been frozen. The stock market is plummeting. In the wake of these events, riots in the country's city streets are a common occurrence.

The table below presents real GDP and consumer prices data for

Argentina

from 1994 to 2002. It reveals robust growth (except for 1995)

from

1994 until the recession of 1999 (which actually originated in late

1998).

Consumer prices rose modestly until deflation appeared in

1999.

The data for 2002 are the IMF's World Economics Outlook (April)

preliminary

estimates, and they are very problematic. (Note: The IMF

economic

analysts had not seen the dramatic rise in consumer prices in April).

|

|

(annual % change) |

(annual % change) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

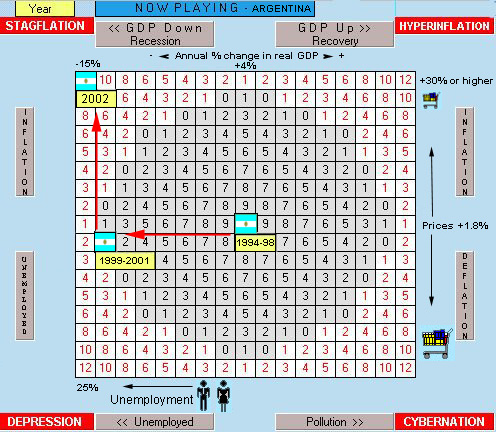

The image below presents Argentina's macroeconomic performance on the playing field of The Global Economics Game. It shows the Goldylocks-like economy from 1994 to 1998, the three year recession from 1999 to 2001, and the dramatic soar to stagflation that appears to be occurring this year. [Editor's note: When an economy's flag moves from right to left on the playing field, it indicates an economic slowdown or recession. Cyclical unemployment increases when an economy's production slows down or declines. Moving up the playing field indicates inflation. The numbers in the playing field indicate a country's score as it attempts to balance growth, pollution, inflation, and unemployment. Black numbers are positive; red numbers are negative. The objective is to land in or near the center square. The worst possible locations for an economy to be are in the corners of the playing field. These placements of Argentina on the playing field based on IMF statistics are only approximations.]

The Microeconomic Consequences of Macroeconomic Performance

By their very nature, unfavorable macroeconomic performance statistics tend to dehumanize and depersonalize the daily frustrations of households and businesses coping with the adversity. Instead, the personal microeconomic consequences of negative macroeconomic performances are found in people's diaries, biographies, novels, and artistic expressions of the period. People sing the blues. Steinbeck writes "The Grapes of Wrath." Anyone who has read Steinbeck's novel depicting the plight of the Joad family during the 1930s Great Depression in United States can understand and empathize with economic despair.

Rising cyclical unemployment that accompanies recession and depression means that there are more job seekers than there are jobs to be found. It becomes a game of musical chairs. There are more players than chairs, and when the music stops some players are left standing (i.e., unemployed). Imagine being a recent college graduate seeking employment in Argentina. At every attempt you would hear that your knowledge and skills are not demanded at this time. "Our company is not hiring," you would be told. "We are laying off workers." Large and small businesses in Argentina are not maximizing profit. They are minimizing losses. In the long run, many businesses will have failed. Investment in new capital is irrational. Budding entrepreneurial hopes are dashed. Innovation seems pointless.

Inflation is most pernicious. It is an invisible thief. It robs households of their wealth more skillfully than a professional thief in the night. When prices rise faster than incomes, rational households find themselves maximizing less and less total utility. (In the vernacular of advanced microeconomics, households find themselves on lower and lower indifference curves). Imagine a family in Argentina that earns 4,000 pesos per year and has managed to save 20,000 pesos. If inflation skyrockets to 10% per month, the average annual rate compounds to 213%! The family's income and wealth adjusted for 213% inflation become the following in real terms: The family is now earning the equivalent of 1,278 pesos in terms of purchasing power. Their savings has dwindled to 6,390 pesos. Almost overnight, the family has been robbed of nearly 70% of its wealth.

Currency markets quickly recognize the effects of inflation and factor them into the exchange rate accordingly. When the exchange rate between the Argentine peso and the US dollar was 1 to 1, the family's pesos were equivalent to US dollars. Today, the Argentine peso that was worth US $1 (less than a year ago) is only worth about US $0.27 in the foreign exchange market; and it continues to fall daily.

A currency ravaged by inflation becomes like a hot potato. No one wants to hold it. Peso denominated assets such as Argentina's publicly held stocks are dumped as quickly as possible. They are converted into pesos, and then the pesos are converted into almost any other currency or almost anything tangible. The first half of this year the Merval stock index lost approximately 75% of its value due to panic selling. Pension funds and family investment stock portfolios have been virtually ruined. The lyric "Don't Cry For Me, Argentina" would aptly be followed with "Cry For Yourselves."

Latin America and Argentina Stock Indexes

Source: Latin

Focus.

(Image reproduced with permission).

Ideological 'isms, Pragmatism, and Policy Blunders

It

is, perhaps, unfortunate that Argentina's economic collapse has

occurred

within the context of its attempts to implement more market-oriented

reforms.

It gives the critics of capitalism ammunition. Marxists will say

that it proves once more that capitalism exploits the working class and

leads ultimately to poverty and despair for the masses.

Socialists

will say it was obviously a mistake to abandon planned socialism.

Cynics will predict fascism. The followers of Joseph Schumpeter

will

say that it exhibits the inherently destructive nature of a capitalist

system that is never in equilibrium. Keynesian economists will

say

that it reveals capitalism's proclivity to find equilibrium at less

than

full employment. Anti-globalists will blame freer trade.

Modern

neo-classical economists will be put on the defensive to explain how

greater

reliance on free market forces could not lead to such disaster.

It

is, perhaps, unfortunate that Argentina's economic collapse has

occurred

within the context of its attempts to implement more market-oriented

reforms.

It gives the critics of capitalism ammunition. Marxists will say

that it proves once more that capitalism exploits the working class and

leads ultimately to poverty and despair for the masses.

Socialists

will say it was obviously a mistake to abandon planned socialism.

Cynics will predict fascism. The followers of Joseph Schumpeter

will

say that it exhibits the inherently destructive nature of a capitalist

system that is never in equilibrium. Keynesian economists will

say

that it reveals capitalism's proclivity to find equilibrium at less

than

full employment. Anti-globalists will blame freer trade.

Modern

neo-classical economists will be put on the defensive to explain how

greater

reliance on free market forces could not lead to such disaster.

But while academia debates the efficacy of alternative economic systems, Argentina's government has the responsibility to implement pragmatic policies to get the economy out of its mess and back on a track of sustained growth without inflation. Some will suggest that doing something is better than doing nothing. Others will say that doing nothing would be better than doing something wrong. Bad economic policy can be worse than no policy.

While its doubtful that Argentina's government can be held responsible for the recession in 1999, a strong case can be made for the notion that Argentina's government is at least partially, if not wholly, responsible for this year's economic catastrophe.

The critical moment came in December of last year when it became obvious that Argentina was going to default on its external debt. After a period of debt refinancing at escalating interest rates, Argentina's debt service ratio (interest plus amortization divided by merchandise exports) became unmanageable. Official reserves were depleted to protect the fixed exchange rate between the peso and the US dollar. The IMF refused to loan any more reserves without a fiscal austerity plan for Argentina. Capital flight ultimately unhinged the fixed rate arrangement, and Argentina was forced to devalue the peso in January.

There is some merit to the argument that allegiance to the fixed exchange rate system was a policy mistake. It's virtually impossible for a government to maintain a fixed exchange rate when fundamental economic forces cause its currency to be overvalued. In the case of Argentina, monetary policy became de facto restrictive and exacerbated the economy's recessionary trend at the same time that ill-advised and ill-timed tax increases implemented early in 2000 were a fiscal drag on the economy. Exchange rate, monetary, and fiscal policies combined to assure an "L" shaped recession.

However, Argentina is not the first economy to experience recession. It is not the first country to default on external debt; and it's not the first country to necessarily abandon a fixed exchange rate. (Nor will it be the last). The key question is: What else should a government do (and not do) as it lets the foreign exchange market depreciate its overvalued currency while its economy is in recession? Argentina's answer to this question was to commit a panic driven policy blunder that has resulted in this year's economic chaos: It froze bank deposits and transfers of funds abroad. It converted all dollar deposits to pesos. It literally locked people out of their own banks, took control of private household and business savings, and proceeded to spend the savings on government programs. It was a mistake of monumental proportions, because it undermined the very system it was trying to defend -- namely, the money and banking system of Argentina.

Money is whatever people say it is. Fiat pesos will not

function

well as a medium of exchange if there is no faith in them, and

Argentineans

have good reason to distrust their pesos. Historically, they have

had recurring bouts with hyperinflation. Now they are in a

situation

where they can't even access their own depreciating pesos!

However,

peso depreciation in the foreign exchange market isn't causing

inflation.

It's the other way around. Inflation is causing the peso to

depreciate,

and inflation is being caused by too many government controlled pesos

to

pay for public goods and services, a bloated civil service,

entitlements,

and interest on its public debt. It's a classic case of

monetization.

Argentina's government is now giving people a choice between being

frozen

out of their savings or accepting newly issued peso denominated

government

bonds (IOU's) in exchange for their private savings accounts.

Either

the government is already effectively "printing" the pesos to pay for

its

deficit spending or the public is expecting it to do so. In

either

event, there are now too many pesos perceived to be chasing too few

goods

because the economy can't physically produce more private goods and

services

as quickly as the pesos are being injected into a paralyzed

economy.

There is no more trust in the peso. To fix this crisis in

confidence,

Argentina needs either a good economist, a magician, or both.

The Magic Policy: Dollarization?

Kurt Schuler, senior economist at the Joint Economic Committee of the U.S. Congress, published a scathing indictment of Argentina's recent economic policies at the Cato Institute in July. In his comprehensive policy analysis entitled Fixing Argentina, he wrote: "Argentina's currency crisis and economic depression have been caused by the bad policies of its government -- not by banks, speculators, the International Monetary Fund (despite the bad advice it has given), or other scapegoats. The Dela Rua and Duhalde governments have made several gigantic blunders, namely, increasing tax rates, freezing bank deposits, devaluing the peso, and forcibly converting dollar bank deposits and contracts into pesos ('pesofication')." Schuler proposes that the most immediate steps necessary to restore economic health to Argentina are: (1) "to officially dollarize, converting all peso assets, liabilities, and prices into dollars; (2) to the extent possible, reverse the damage done by pesofication of deposits; (3) reconstruct the financial system; and (4) drastically reduce tax rates."

Dollarization is an intriguing proposal, and it might be the magic policy Argentina desperately needs. At the very least, it would restore monetary stability to Argentina -- a necessary, if not sufficient, condition for recovery. However, it would essentially turn monetary policy in Argentina over to the U.S. central bank. Governments are reluctant to relinquish sovereignty over their currency and banking system to an external entity. Of course, if the government of Argentina could be trusted with monetary control over the peso, then dollarization would merely be redundant. However, the most undesirable alternative is to perpetuate the current policy blunders that border on criminal. Because nobody trusts the peso, nobody is doing anything to save and invest in Argentina's future. Until that changes, Argentina's outlook will remain bleak.

Image is the property of NVTech

Sources and Recommended Links

http://www.latin-focus.com/countries/argentina/argentina.htm

"What Happened to Argentina?" by Mark Weisbrot and Dean Baker (January 31, 2002)

"Fixing Argentina" by Kurt Schuler: http://www.catoinstitute.com/pubs/pas/pa-445es.html

http://www.cia.gov/cia/publications/factbook/