December

29, 1999 -- Earlier this month the World Bank released its publication

Global

Economic Prospects and the Developing Countries 2000. It

predicts a gradual economic recovery for South America.

Argentina,

Brazil, Chile, Colombia, Ecuador, and Venezuela were all experiencing

recession

by the fourth quarter of 1998, and they all got worse in 1999.

December

29, 1999 -- Earlier this month the World Bank released its publication

Global

Economic Prospects and the Developing Countries 2000. It

predicts a gradual economic recovery for South America.

Argentina,

Brazil, Chile, Colombia, Ecuador, and Venezuela were all experiencing

recession

by the fourth quarter of 1998, and they all got worse in 1999.

The World Bank's cautious optimism for the region's recovery in the year 2000 (and beyond) is contingent upon the occurrence of several key events. First, it is assumed that there will be an acceleration in world trade, which helps countries whose exports are a significant percentage of GDP. That is true for Chile (27.5%), Ecuador (25.3%), Uruguay (21.9%), Venezuela (20.0%), and Bolivia (19.7%). Second, commodity prices (oil and metals) are expected to stabilize and/or rise somewhat. Incomes rise and the terms of trade improve for countries whose export prices rise in general relative to other goods and services. Oil prices are especially important to Colombia and Ecuador, and metals prices are significant for Chile and Bolivia. Third, it's anticipated that global capital funds will begin returning to the region. Foreign savings are a major source of investment capital for these countries. Greater exchange rate stability for a number of countries would help to attract foreign investors. So would economic recovery, low inflation, and political stability.

The South American economies were spill over victims of the Asian currency crisis and global economic downturn in 1998 and 1999. Brazil, the largest economy in the region, was forced to devalue its currency (the real) nearly one year ago. That hurt export sales in some of the other South American countries, because the price of their competing export products effectively became more expensive relative to those in Brazil. At the same time, commodity prices in general fell worldwide, thereby reducing the export earnings of many South American countries. The demand for commodities is often relatively inelastic, which means that when prices fall the percentage increase in the quantity sold does not increase by as much as the percentage reduction in price. Therefore, the total monetary value of sales falls!

The annual GDP (adjusted for inflation) turned negative in 1999 in one South American country after another. Preliminary estimates indicate that economic output will have fallen this year in virtually every country. In some countries the rate of decline will be in excess of 5 per cent. It has been one of the most severe economic recessions in the region's history.

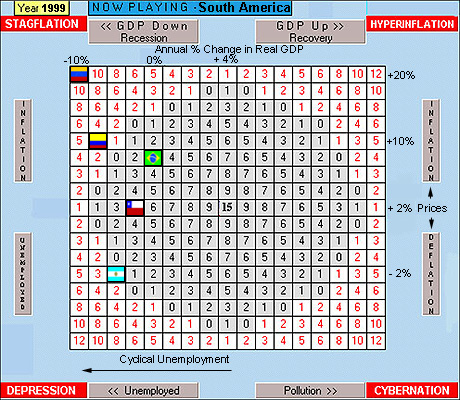

The pictorial below illustrates the playing field of The World Game of Economics and simulates the approximate location and economic performance of South America's five largest economies in 1999. All of the countries moved from right to left during the year, indicating an economic downturn in real GDP. Venezuela and Colombia suffered the most severe economic setbacks, but all five countries are expected to record zero or negative growth for the year.

Four of the five countries have moderate to severe stagflation.

That's a recession combined with inflation. The higher up the

playing

field a country goes, the higher the rate of inflation. It ranged

from nearly 3 percent in Chile to just over 20 per cent in

Venezuela.

Only Argentina escaped inflation and actually experienced deflation

as its price level actually fell by almost 2 per cent. Argentina

appears to be in a more traditional recession where falling demand (as

opposed to supply) has a greater effect on the economy. [Note:

Inter

country comparisons regarding measurements of growth, unemployment, and

inflation can be unusually tricky. Each country has its own

unique

structural pattern and parameters. The degree to which incomes

are

indexed to inflation is an example. Such differences can be

especially

acute where there are various degrees of cultural tolerances, economic

entitlements, health and safety regulations, and a country's stage of

economic

development. The simulation above is merely an approximation and

unrealistically assumes for simplicity that there are little or no

structural

differences among the countries].

Brazil is South America's flagship country and holds the key to the region's future. Its economy is larger than all of the others combined. When it catches a slow wind or a lull, all of the others begin to luff. Recent reports indicate that, hopefully, the worst is over for the Brazilian economy. The World Bank is predicting positive growth for Brazil in the year 2000. The effects of its currency devaluation should continue to generate a positive spending multiplier well into next year. More importantly, foreign capital is beginning to return to Brazil, and its foreign exchange reserves have stabilized and modestly risen in recent months.

Shown below are two customized versions of Current Events cards adapted from The World Game of Economics. (Similar cards actually appear in the game). They illustrate that foreign investment is a critical factor for the near term performance and future long-term development of any country. When financial capital fled South America beginning in 1998, the economies in the region began to contract. If foreign financial capital returns to South America in the year 2000, it will help the region recover.

..........

..........

LDCs typically have low domestic savings ratios, and many are saddled with a relatively heavy external debt burden. They are short on capital. Yet capital formation and investment is necessary for the development of infrastructure, education, and rising productivity. Global funds from industrialized countries are the main source of capital for LDCs, but foreign investors will tolerate only so much risk to seek a high return. It's a delicate balance because risk and yield are directly related, but safety and return are inversely related. High inflation and political instability are the two most lethal deterrents to foreign investors. That is, foreign investors will pull their funds out of countries that have high inflation and/or political instability. That's why it is so imperative that South American countries contain inflation, end political corruption, and provide some degree of safety to foreign investors. Maintaining a relatively stable foreign exchange market is also important to minimize that element of risk for both direct foreign investors and portfolio lenders.

While an economic recovery is expected for the near term, the World Bank's 2000 publication indicates that their analysts are concerned about problems facing the region on the long term horizon. The following is an excerpt from the Bank's report: "Output growth for the (Latin American) region in the long term is now projected to average 4.2 per cent., which is a reduction of [0.2] percentage points compared to Global Economic Prospects 1998/99. The lower forecast is based on several factors which, although characteristic of the region for many years, have become more evident during 1999. National saving rates in several large countries have not risen in the 1990s and most continue to rely on foreign savings to accommodate increases in investment. High external indebtedness has increased reliance on international capital markets to finance debt repayments, and there is increasing evidence of reform fatigue in a number of countries."

These are not exactly stellar comments, and we can only hope that

the

good people and leaders of the South American countries consider them

seriously.

While portions of this article have discussed the region's economy in

the

context of a computer game, economic life for individuals and

households

is much more than that. Economics, after all, is about policy

decision

making in a world of scarce resources and opportunity costs. Bad

policy costs more than good policy, and the future quality of life for

more than 300 million South American citizens is at stake.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Recommended Link: The World Bank