April

24, 2000 The International Monetary Fund (IMF) released its

spring

World

Economic Outlook report earlier this month, and it would appear

that

the near term prospects for the global economy are indeed bright.

"All areas of the world economy are contributing to the strengthening

and

growth prospects going forward," stated Graham Hacche, IMF Deputy

Director

of External Relations, within minutes of releasing the much anticipated

report. "The picture for global growth is strong and quite

positive

for year 2000, and we believe beyond," he stated at the April 12 press

conference in Washington, D.C.

April

24, 2000 The International Monetary Fund (IMF) released its

spring

World

Economic Outlook report earlier this month, and it would appear

that

the near term prospects for the global economy are indeed bright.

"All areas of the world economy are contributing to the strengthening

and

growth prospects going forward," stated Graham Hacche, IMF Deputy

Director

of External Relations, within minutes of releasing the much anticipated

report. "The picture for global growth is strong and quite

positive

for year 2000, and we believe beyond," he stated at the April 12 press

conference in Washington, D.C.

Contributing to this cheerful outlook were the following developments in 1999: (1) The United States and Canada continue to show unprecedented economic strength; (2) The United Kingdom is also experiencing its longest economic expansion on record; (3) The Asian economies have undergone a rapid and remarkable turnaround from the '97-'98 recession, and this is bolstering Europe's economic recovery; (4) Even some of the Latin American economies are beginning to rebound from one of the region's worst recessions.

The IMF's spring report routinely summarizes the previous year's macro economic performance of the world's economies and then ventures into the precarious forecasting arena. Overall, world GDP grew at 3.3 per cent in 1999, and the IMF is forecasting 4.25 per cent growth for year 2000. That's above the long-term average growth rate of just under 4.0 per cent. Global inflation is at its lowest level in over thirty years and is expected to be held in check by productivity gains and monetary restraint in the industrialized countries. The recent surge in oil prices is not expected to contribute much to global inflation, especially since OPEC recently agreed to increase production in the months ahead and oil prices have dropped from their peak in March. However, the report identifies several important risks to the global economy including the possibility of an economic slowdown in the United States and the uncertainties associated with fluctuating equity prices.

When asked about the accuracy's of past IMF forecasts, Fleming Larsen, Deputy Director of IMF Research, reflected the humility he has acquired from his many years of experience at attempting to predict the future. "Forecasting is a very difficult business," he answered. "The world business cycle is subject to a huge degree of uncertainty, the turning points are notoriously difficult to predict, and this is an experience that is shared by basically all forecasters. It does require, I think, a degree of flexibility and willingness to change the course of policies when required by unexpected economic developments."

Fleming Larsen's remarks capture the essesence of The World Game of Economics. Countries move around the playing field of the game as the global economy unpredictably shifts direction. One year your economy can be performing near the center of the playing area, and the next year your economy can be hurling toward depression or inflation. The objective of the game is to use the appropriate policies at your disposal to correct for a given economic imbalance. The remainder of this article highlights the IMF's World Economic Outlook using the playing field of the game as a way to visually depict the relative performance of the world's individual economies in 1999 and the IMF's forecast for the year 2000.

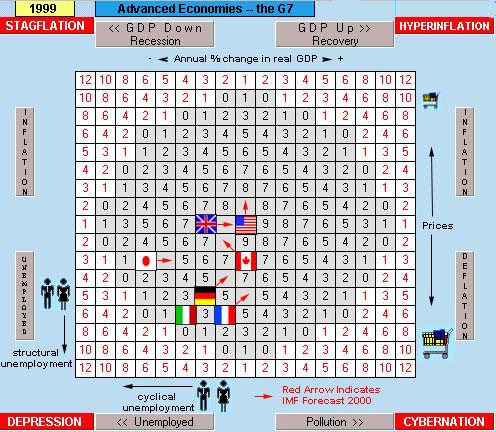

The Largest Industrialized Nations: The performance of the global economy is most significantly influenced by the seven largest industrialized countries. They are called the G7, and they account for the bulk to the world's production and trade. The United States is the largest of these countries. Its GDP is more that twice the size of Japan, which is the second largest economy in the world. In 1999 the US economy grew by just over 4 per cent, while Japan continued to languish in recession. Canada demonstrated unusually strong growth last year, and the United Kingdom sustained an unprecedented economic recovery in terms of longevity. The Western European countries Germany, France, and Italy continue to be plagued by structural unemployment, and the IMF report recommends policies to improve labor mobility in the region.

The image above depicts the playing field of The

World Game of Economics and the relative economic performance

of

the G7 countries in 1999 implied by IMF statistics and forecasts.

The further to the right a country/flag goes, the faster the rate of

growth.

The very center is approximately 4 per cent real growth. When a

country

moves to the left of the playing field, the economy's rate of

growth

slows down and it can slip into recession (as in the case of

Japan).

Declining GDP causes cyclical unemployment. Structural

unemployment

appears when a country moves down the playing field. Generally,

the

higher up in the playing field a country goes, the higher the rate of

inflation.

The middle of the playing field is assumed to be approximately 2%

annual

inflation. Differences in the natural rate of unemployment for

different

countries can cause incongruities regarding inflation and unemployment

trade-offs. Placement of countries on the playing field based on

IMF statistics is only an approximation.

|

|

1999 |

2000 |

1999 |

2000 |

1999 |

2000 |

1998 |

1999 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

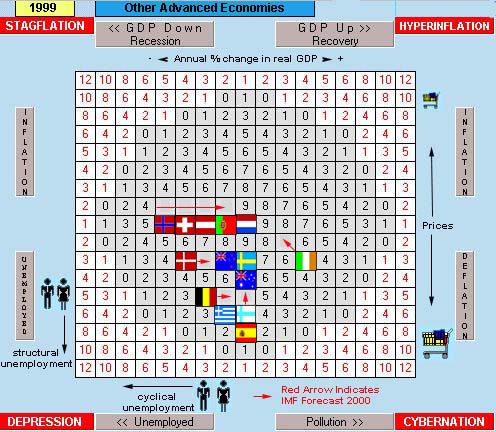

Other Advanced Countries: The Netherlands was one of the top performing countries in the world in 1999 in terms of balanced growth, environmental quality, inflation, and unemployment. Portugal recorded a good economic performance for the second consecutive year, but its neighbor country Spain has one of the highest (structural) unemployment rates in the world. Ireland is the fastest growing country in Europe. The combinations of structural unemployment in Spain and Finland, rapid growth in Ireland, and slower growth in Austria and Belgium create potential policy problems for the E-11 and the new European Central Bank. Australia and New Zealand both experienced relatively good economic performances last year, but inflation is predicted to accelerate this year. Although inflation is creeping upward, most of the countries in this grouping are expected to improve their economic performance in the year 2000 in terms of growth and unemployment.

|

|

1999 |

2000 |

1999 |

2000 |

1999 |

2000 |

1998 |

1999 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

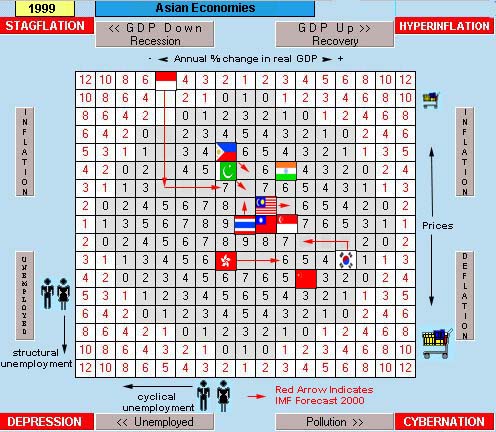

The Asian Economies: Perhaps the most significant development in 1999 was the speed and degree to which the smaller Asian economies rebounded from the financial and economic crisis of 1997-98. Korea has returned to be one of the fastest growing economies in the world. In 1998 Korea's real GDP fell by nearly 7 per cent. In 1999 it grew by nearly 11 per cent! The other newly industrializing countries (NICs) in the Asian region also registered rapid growth rates in 1999. Hong Kong's economy, for example, declined by over 5 per cent in 1998 and grew by nearly 3 per cent in 1999. The IMF report forecasts the island's growth rate to be 6 per cent in 2000. Indonesia is predicted to demonstrate the greatest economic improvement in 2000, primarily in terms of growth and lower inflation. Annual inflation in Indonesia was nearly 60 per cent in 1998! It decelerated to about 20 per cent in 1999, and is forecast to fall to 3.5 per cent in the year 2000. China's economy continues to grow at just over 7 per cent annually. China experienced deflation in 1999.

Rapidly growing economies like those in the Asian region tend to experience severe environmental and social problems. Pollution, crime, congestion, and social dislocations are all on the rise. Inequalities of internal income distribution tend to accompany rapid economic growth, generating social disharmony and political instability. Dealing with these problems and issues promises to be one of the great challenges for these governments in the 21st century as the Asian economies continue to exhibit rapid growth and industrialization.

|

|

1999 |

2000 |

1999 |

2000 |

1999 |

2000 |

1998 |

1999 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

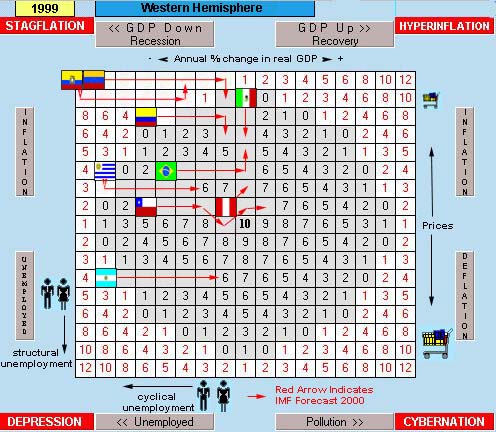

The Western Hemisphere: One of the most welcome surprises of 1999 was the early signs of economic recovery for some of the countries in Latin America, most notably Brazil and, later in the year, Argentina. Except for Mexico and Peru, the region is struggling with one of its worst economic recessions on record. The IMF report forecasts positive economic growth for virtually every economy in this region in 2000. However, inflation and the threat of stagflation pose potential future problems for the area. Brazil's inflation rate is forecast to climb to 7 per cent; Mexico, Ecuador, and Venezuela are all predicted to have double-digit inflation this year. Inflation arbitrarily redistributes real income and wealth, distorts economic decision-making, and undermines the effectiveness of capital markets.

|

|

1999 |

2000 |

1999 |

2000 |

1998 |

1999 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Selected Economies: Contributing to the bright economic outlook for the global economy in 2000 are other countries around the world that appear to be improving their economic performance in terms of growth, unemployment, and inflation. South Africa, Nigeria, Saudi Arabia, and Israel are all forecast to perform better this year than last year. Falling oil prices in 1998 and early 1999 retarded growth in the oil exporting countries, but rising oil prices over the past twelve months are expected to reverse that trend. Russia's economy grew by 3.2 per cent last year, and the IMF forecasts disinflation in Russia from 86 per cent in 1999 to 20 per cent this year. Turkey suffered from very severe stagflation in 1999 but is expected to experience positive economic growth this year.

|

|

1999 |

2000 |

1999 |

2000 |

1998 |

1999 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Summary: The objective in The World Game of Economics is to land in or near the center of the playing area as frequently as possible. That represents a balance of macroeconomic performance goals in terms of growth, pollution, unemployment, and inflation. It is difficult to accomplish this both in the game and in the real world, as one can surmise from the above presentation of recent economic data for nations around the world. If it were easy, more countries would perform better more often and more consistently. However, it does appear from the IMF's report that most countries are in the process of improving their economic performance and the global outlook for 2000 is a brighter one than last year.

Recommended Link: International Monetary Fund Home Page. http://www.imf.org