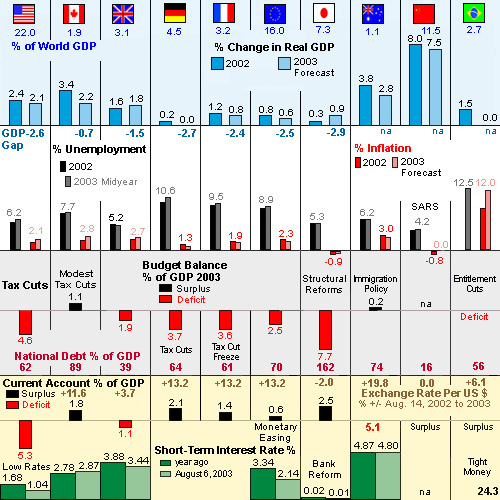

Chart 1: Economic Indicators - Selected Countries

Sources: IMF. World Economic Outlook (April 2003) and

The

Economist magazine (August 9-15, 2003)

August

15, 2003 With each passing week and month the prospects for a global

economic

recovery later this year and in 2004 become more favorable. Where

possible, policy makers are applying Economics 101 cures for

recession:

Tax less, spend more, and lower interest rates. These are

textbook

stimulative polices designed to get a slow moving economy out of its

doldrums.

August

15, 2003 With each passing week and month the prospects for a global

economic

recovery later this year and in 2004 become more favorable. Where

possible, policy makers are applying Economics 101 cures for

recession:

Tax less, spend more, and lower interest rates. These are

textbook

stimulative polices designed to get a slow moving economy out of its

doldrums.

The United States is going to run its biggest fiscal deficit on record this year -- estimated to be over $455 bn and approximately 4.6% of its GDP. Part of this deficit is structural, caused by low tax receipts in a weak economy. However, much of it is deliberate and discretionary as a result of tax cuts and spending increases related to the Iraq war. Congress passed another $350 bn tax relief bill in May that will induce more private sector spending next year and beyond. Monetary policy in the United States has been easing since January 2001, and short-term interest rates have fallen to levels not seen since the early 1950s. Over the past 12 months, the U.S money supply has increased by 7% (exceeding the monetary rule of 3-4%). The 3-month money market rate dipped to 1.04% on August 6.

The European Central Bank (ECB) has finally decided that it's time to help pull Europe out of its doldrums. The broad based money supply has increased by 8% over the past year, and the European 3-month money market rate has dropped by one full percentage point from 3.34% to 2.14%. In June Germany's Chancellor Gerhard Schroeder proposed an 18 bn euro (US $20.6 bn) cut in income taxes early next year to turn the German economy away from the recession toward which it is heading. The German economy is not expected to grow at all this year. According to Schroeder, a 10% reduction in income taxes will increase household consumption by 10%. In order to avoid problems with the European Monetary Union's (EMU) Stabilization and Growth Pact (SGP) that prohibits deficits from exceeding 3% of GDP, Schroeder plans to offset the tax cuts with subsidy cuts and the sale of government held equities in ex-state monopolies. On balance, the proposal is probably stimulative.

In order to avoid problems with the EMU's SGP, France has put a freeze on further tax cuts. At 3.6% France's fiscal deficit already exceeds the 3% rule. However, earlier tax cuts have been set into motion and should help persuade, if not propel, the French economy forward assuming people spend more when they have more income to spend as textbook economics suggests. Elsewhere in Europe, there are problems. Relatively high wage rates in the Netherlands make it less competitive than its trading partners, and the Dutch economy depends largely on exports for economic growth. Italy's economy is projected to grow less than 1% this year and less than 2% next year. The entire Euro area is not expected to recover rapidly unless lower interest rates act quickly to induce investment spending. Expansionary monetary policy may be able to successfully ward off or diminish the intensity of a recession, but it can be painfully slow to bring about a recovery.

That's why fiscal tax cuts, spending increases and deficits are so important at this juncture. Europe is somewhat fiscally handcuffed by its SGP. It's not that the countries in the EMU can't deficit spend. They can, and they do. It's that they can't deficit spend beyond 3% of their GDP's. Therefore, fiscal stimulus in Europe is less so than it might otherwise be.

Likewise, Japan (the world's third largest economy and major exporter) is hampered by its inability to inject any more fiscal or monetary stimulus into the economy. Japan's fiscal deficit already exceeds 7% of GDP; and its gross federal debt is 162% of GDP -- the highest in the world among the industrialized countries (ICs)! Interest rates in Japan are just slightly above 0%. Put simply, Japan has run out of both fiscal and monetary options. There is a glimmer of hope that Japan's structural reforms and anti-deflationary moral suasion will begin to awaken Japan from its 10+ years of slumber. This year's first quarter report indicated that Japan's economy grew by 2.6% (average annual rate).

In other parts of the world, things are looking slightly better. The United Kingdom, Canada, and Australia are doing reasonably well. They are in the early stages of economic recovery. The U.K is modestly deficit spending. Canada and Australia are running small budget surpluses. There is room for further stimulus; but they are all somewhat impaired and reluctant to do so, because their inflation rates at nearly 3% are relatively high among the ICs.

China (the world's second largest economy), the Asian tigers (Hong Kong, Taiwan, Singapore, South Korea), and India are all sailing along. Most have growth rates exceeding 4% annually. These countries grow, not so much because of fiscal or monetary stimulus, but because of supply side resource and productivity gains associated with privatization, direct foreign investment, export promotion strategy, and capital deepening. These are secular or long-term, as opposed to cyclical, trends that are expected to continue in the decades ahead. They are vulnerable to non periodic capital flight and currency crises, but they generally maintain sound fiscal and monetary practices to contain inflation.

Unfortunately, this cannot be said of Central and South America. Their inflation and debt problems continue to plague their economic performances. Brazil, the largest economy in the region, is headed directly for stagflation. Venezuela is already there. The Venezuelan economy shrank by 29% in the first quarter of this year, while inflation galloped in excess of 10%! It is the worst performing economy among the emerging market economies. On the other hand, Mexico is fairing somewhat better. The Mexican economy is growing slightly above 2%, and inflation is just below 5%.

Some of the global trends discussed above are displayed in Chart 1 below. It shows recent key economic indicators and forecasts for nine selected countries and the Euro area. China is the fastest (7.5%) growing economy in the chart. Unemployment among the ICs is highest (10.6%) in Germany. Inflation is highest (12%) in Brazil. Zero growth, 12% unemployment, and 12% inflation qualifies as stagflation for Brazil. Japan and China both have recently experienced deflation. The United States and Japan have the highest budget deficits as a per cent of GDP. Japan has the highest national debt expressed as a per cent of GDP. The United States runs a chronic current account deficit on its balance of payments. China runs a chronic surplus. The US dollar has been depreciating against all the other currencies except the Japanese yen and the Chinese yuan over the past year. Short term interest rates are lowest in Japan and the United States, but they are falling in Europe.

Chart 1: Economic Indicators - Selected Countries

Sources: IMF. World Economic Outlook (April 2003) and

The

Economist magazine (August 9-15, 2003)

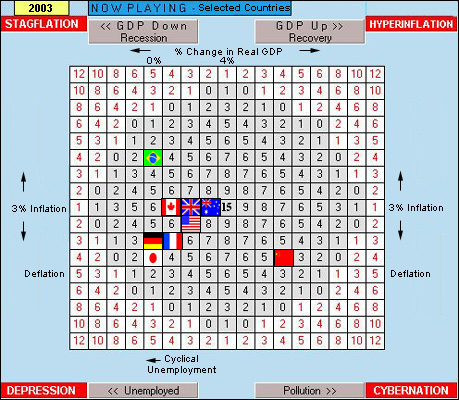

The image below presents the macroeconomic performance of these countries on the playing field of The Global Economics Game. It reveals that most of the economies are expected to experience less than 4% growth in 2003. Brazil, Germany, and Japan may not grow at all this year. Japan and Germany qualify for a traditional recession. Brazil, on the other hand, is in stagflation. China's economy is the only one growing rapidly and without inflation. Australia is the overall best performing economy in the field. Its growth rate (2.8%) is higher than the U.K.'s (1.8%), and its unemployment rate (6.2%) is lower than Canada's (7.7%).

[Editor's note: When an economy's flag moves from left to right on the playing field, it indicates accelerating growth. When it moves from right to left, it indicates an economic slowdown or recession. Cyclical unemployment increases when an economy's production slows down or declines. Moving up the playing field indicates inflation. Moving down the playing field indicates disinflation or deflation. The numbers in the playing field show a country's score as it attempts to balance growth, pollution, inflation, and unemployment. Black numbers are positive; red numbers are negative. The objective is to land in or near the center square. The worst possible locations for an economy to be are in the corners of the playing field. The placements of the countries on the playing field based on IMF statistics and The Economist's consensus forecasts are only approximations.]

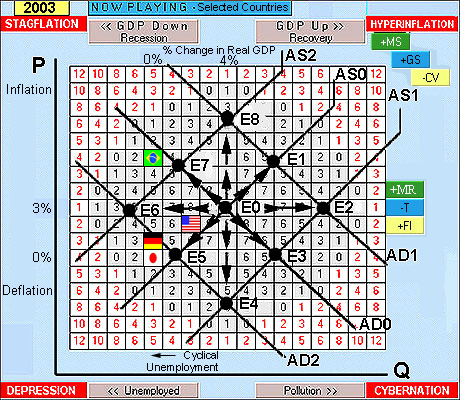

The game assumes that a country's position on the playing field is being determined by the short-run equilibrium of aggregate demand and aggregate supply. This macroeconomic model is at the heart of contemporary macroeconomic principles and theory. There is, at least, one chapter on this model in virtually every principles textbook used at colleges and universities in the world. The aggregate demand curve is inversely related to the general price level (P). Aggregate expenditures (Q) = (C+I+G+X) increase as the price level falls, ceteris paribus. The aggregate supply curve is directly related to the general price level. P and Q move up and down together along the aggregate supply curve. The production of goods and services increases when prices rise (and vice versa), ceteris paribus. Changes in aggregate demand cause the curve to shift outward (to the right) or inward (to the left). Changes in aggregate supply cause the curve to shift outward (down) or inward (up). This model is superimposed on the playing field of The Global Economics Game" in the image below.

An economy would ideally be in equilibrium at E0. However, if aggregate demand (AD) were to fall, then the aggregate demand curve would shift from AD0 to AD2 and the economy would move toward E5. This is precisely what has happened to Germany and Japan (and to a lesser degree the United States). On the other hand, if aggregate supply (AS) were to decrease, then the aggregate supply curve would shift from AS0 to AS2 and the economy would move toward E7. This has happened to Brazil.

Macroeconomic Policy Tools

The traditional demand side macroeconomic policy tools to get out of a recession or depression are divided into fiscal, monetary and foreign. Fiscally, the appropriate policies are to increase government spending [+GS] or cut taxes [-T]. Increasing government spending directly increases aggregate demand. There is a multiplier effect, and total spending and income ultimately increase by more than the initial increase in government spending. Cutting taxes indirectly increases aggregate demand by giving households more disposable income. Supply side economics suggests that cutting taxes also increases aggregate supply by encouraging harder work and entrepreneurial risk taking for greater after-tax income.

The appropriate monetary polices to ward off recession are to increase the money supply and lower interest rates significantly [+MS] or a little [+MR]. Adding liquidity to a nation's banks through central bank open market purchases of government securities raises bond prices and lowers interest rates. This induces increased borrowing and investment spending by businesses and increased consumer spending for durable goods on the part of households.

In foreign policy, a currency depreciation [-CV] increases net exports by making exports cheaper to foreigners and imports from foreigners more expensive. Assuming the elasticity of demand is relatively elastic (and it ultimately becomes so with price increases), then a country that deliberately depreciates its domestic currency through central bank intervention in foreign exchange markets will observe an increase in net exports of goods and services, ceteris paribus. Attracting direct foreign investment [+FI] is another way to increase both aggregate demand and aggregate supply. This can be done by removing impediments to foreign investors who wish to locate or expand their business operations in your country.

Overall, the objectives of macroeconomic policies when an economy is in or headed for a recession are to increase aggregate demand and/or supply without causing too much inflation. However, implementing these polices in the real world is more difficult than it would seem to be at first blush. First, there is the problem of timing. It's not always clear where the economy is or where it's headed in the immediate future. There's always an information or recognition lag. The free market forces of aggregate demand and aggregate supply can be capricious. An ill timed, misdirected policy can be worse than doing nothing.

Second, fiscal policy is charged with political polemic and subject to policy gridlock. For example, discretionary deficit spending is universally understood to be stimulative. But whenever tax cuts are suggested, critics drag the discussion into normative debate on judgments of equity and fairness. They exclaim that tax cuts benefit only the rich and that's not fair. A democratic government can debate tax equity indefinitely.

Third, there are different budget philosophies. The annually balanced budget and the notion that governments shouldn't deficit spend at all is a widespread, popular belief. A more sophisticated and accurate criticism of deficits is that they crowd out the private sector if the government deficit spends when the economy is already at full employment and there is no corresponding or concomitant increase in potential GDP. When the government deficit spends, it has to borrow more money. If the money supply stays constant, then interest rates rise; and this causes private investment and consumption to fall. This is called the crowding out effect. If the deficit is monetized with accommodating increases in the money supply, then the economy gets inflation. As a borrower and spender, the government wins in an inflationary spiral; as lenders and savers, businesses and consumers lose. Either way, the government sector crowds out the private sector of a market economy if the government deficit spends at full employment.

Fourth, monetary policy has problems of both timing and asymmetry. Monetary policy can usually be implemented quickly. At a recent congressional hearing the chairman of the U.S. central bank, Alan Greenspan, testified that he could act within 15 minutes of recognizing a clear and present danger. The problem with monetary policy is that the timing of its effects are not all that well known or understood. The decision linkages between the time the central bank adds liquidity and the multiplier effects of increased spending by business and consumers are irresolute and unpredictable. Some economists believe that the effects of a given monetary policy can take a year or longer to manifest themselves. It is also generally understood that monetary policy is more effective at curtailing demand pull inflation than it is at generating an increase in aggregate demand when the economy is heading toward a recession for reasons quite apart from the cost of money. Stated differently, monetary policy can probably reign in an economy; but it may be weak or ineffectual at getting an economy to move forward. Japan, for example, has had both low interest rates and recession for a long time.

Fifth, economists are not in agreement on the effectualness of deliberate currency interventions. Currency depreciations that are sterilized by corresponding tight monetary polices to avoid demand pull inflation are especially suspect. The expansionary effects of a currency depreciation are often offset by the contractionary effects of a simultaneous tightening of money to keep interest rates stable. Also, the small volume of currency transacted by a central bank (or even a group of central banks) is dwarfed by the total volume of foreign exchange transactions on a given day. If the foreign exchange market is determined to move a currency in a particular direction, it's not likely that a single central bank can change its direction; and its dubious to believe that a group of central banks could be much more effective. What is being said here is that the ceteris paribus condition, which assumes a neutral monetary policy and a receptive foreign exchange market when deliberately depreciating a currency, doesn't always hold.

Finally, demand side polices are not effective when the problems are on the supply side. This is Brazil's dilemma. If it deficit spends or increases the money supply or depreciates its currency, then it causes still more unacceptable inflation. If it runs a budget surplus or decreases the money supply or appreciates its currency, it exacerbates the recession and cyclical unemployment. Supply side problems require supply side solutions.

Back To the Future

The economies of the United States, Europe, and Japan are either in a recession or having problems with slow recovery and high levels of cyclical unemployment. Nor are the economies of the United Kingdom and Canada robust. That's approximately 50% of the global economy and nearly all of the ICs in the world. Add some of the economies in Middle Europe, most of the Western Hemisphere, a few more countries in Africa and Asia and the total number of countries that are either in recession or not far from it account for nearly two thirds of the global economy.

In light of these trends, why should the prospects for the rest of 2003 and next year be considered favorably biased toward a more rapid economic recovery? The reason is that stimulative macroeconomic policies are being put into motion by key policy makers. The United States is certainly doing its part, and that is of great significance. The U.S. economy is the largest and most influential in the world. It accounts for nearly one fourth of world output and is the world's largest trading nation. If Economics 101 textbook economics has any validity, then the stimulus tax cuts and expansionary monetary policies of the United States should push and pull the U.S. economy forward. If employment and incomes rise in the United States, then American consumers will not only buy more American goods; they will also import more goods and services from the rest of the world. The recent depreciation of the U.S. dollar was not deliberate, but it will expand the U.S. economy at the expense of the others whose currencies have appreciated.

That's why the stimulus actions in Europe are so significant. The ECB's recent shift to an easing of monetary policy and lower interest rates will both stimulate the European economies and reverse or slow the trend of euro appreciation. The German tax cut proposal for 2004 is a most promising development. The German economy is nearly 5% of the world's GDP, and Germany is the largest economy in the EMU. Spain is already doing fairly well cyclically. Together, Germany and Spain could move Europe out of its doldrums early next year.

The crowding out effect is less relevant, because these economies are at less than full employment. The International Monetary Fund (IMF) estimates that the United States, the European Union, Canada, the United Kingdom, and Japan all have negative GDP gaps. That is, their actual GDPs are below their potential GDPs at full employment. And Alan Greenspan has testified that he fears deflation more than inflation. That's why he considers stimulus to be appropriate at this time.

The likely prospects of economic recovery in the United States and Europe combined with optimism, hopeful restructuring in Japan, the relatively strong economies of Australia, China, India, and the Asian tigers adds up to a favorable outlook for the rest of this year and an especially favorable outlook for next year. One must wonder what the outlook would be in the absence of Economics 101 stimulus policies.

Image is the property of NVTech

Sources and Recommended Links

http://www.imf.org/external/pubs/ft/weo/2003/01/index.htm