April

1999 Eleven members of the European Union have moved beyond a

common

market and formed a monetary union with a common currency. Their

new euro currency unit was introduced to the world on January 1, and it

is now used for commercial and banking transactions within the euro

zone.

Euro bank notes, like the one pictured on the cover, will be issued by

the new European Central Bank in Frankfurt and will become the legal

tender

for the region in the year 2002. The bank notes will be

denominated

in 5, 10, 20, 50, 100, 200, and 500 euro units. At that time, the

old national currencies (marks, francs, liras, etc.) will be retired

from

circulation. The new system will resemble the United States,

which

uses the dollar as the common currency among its 50 states.

April

1999 Eleven members of the European Union have moved beyond a

common

market and formed a monetary union with a common currency. Their

new euro currency unit was introduced to the world on January 1, and it

is now used for commercial and banking transactions within the euro

zone.

Euro bank notes, like the one pictured on the cover, will be issued by

the new European Central Bank in Frankfurt and will become the legal

tender

for the region in the year 2002. The bank notes will be

denominated

in 5, 10, 20, 50, 100, 200, and 500 euro units. At that time, the

old national currencies (marks, francs, liras, etc.) will be retired

from

circulation. The new system will resemble the United States,

which

uses the dollar as the common currency among its 50 states.

Many regard this new monetary arrangement in Europe as the most significant event in global finance since the world abandoned the gold exchange system in the 1970s. The euro is expected to be a competitor to the US dollar in the international reserve market.

The driving force behind the new system in Europe is fundamentally economic efficiency. The transactions costs associated with currency exchange will be eliminated. Under the old system, a traveler in Europe would exchange currencies at each border and pay a commission charge on each conversion. It was possible to travel the region and leave with significantly less money even if you didn't actually purchase anything.

More importantly, the new system will effectively price goods and services throughout the region in the euro unit. It will now be possible to easily compare the price of something in Germany to its price in Italy. This price transparency will give buyers an advantage and will force sellers to match the lowest price within the euro zone. Producers will be able to seek the lowest cost inputs of materials and components, and these cost savings will be passed on to consumers. Resources tend to be allocated more efficiently when there is more competition and information about prices and costs is less obscure.

The plan to elevate Western Europe's common market to a highly integrated monetary system with a common central bank and currency was conceived in the 1980s. The Delors Plan was adopted by the Maastricht Treaty in 1989. The treaty was ratified in 1992. The decision to adopt the name "euro" for the currency unit occurred in 1995. The planners knew that policy coordination and cyclical convergence was integral to the success of the plan. In order to be eligible to participate in the European Monetary Union (EMU), countries were required to meet fairly strict standards of performance regarding inflation, interest rates, fiscal deficit spending, and national debt as a percentage of GDP.

Skeptics have criticized the euro plan from two vantage points. Politically, joining the EMU relinquishes national sovereignty over money and banking. This is a major sacrifice for countries with a strong sense of national pride and independence. Economically, critics have argued that the divergence of economic performance within the union could render the plan discriminatory and untenable. Different growth and inflation rates within the union would make it almost impossible to conduct rational monetary and currency rate policies. For example, if Germany was experiencing rapid growth and flirting with accelerating inflation, the correct policy would be to cut the money supply and raise interest rates. However, if Italy was in a recession at the same time, then the tight monetary policy within the union would cause Italy's economy to contract even more.

There was also concern that a given central monetary policy would not affect all countries to the same degree and at the same time. Monetary policy is notorious for having unpredictable time lags and degrees of effectiveness under different economic conditions. If the central bank were to, say, increase the money supply and lower interest rates to combat recession in the region, the policy effect might cause inflation in some countries sooner than it would stimulate some of the more sluggish economies. The countries' performances in the region would undesirably diverge instead of converge.

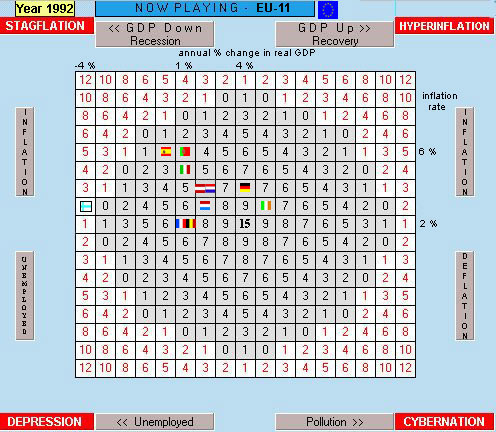

Consider the display below showing the playing field of The World Game of Economics. It depicts the economic performances of the E-11 countries in 1992 with respect to annual growth and inflation. Unemployment rates are deliberately ignored and disregarded. (Unemployment disparities in Europe are largely structural and in that sense immune from monetary polices which affect aggregate demand and cyclical unemployment).

The problem facing policy makers for the E-11 in the above display is that growth rates within the euro zone in 1992 range from -3.6 % in Finland to +5.0 % in Ireland. Inflation rates range from 2.4 % in France to 6.3 % in Portugal. If the central bank were to tighten to curtail rapid growth in Germany and Ireland and to combat inflation in Portugal and Spain, then Finland and France and Belgium would be adversely affected. French farmers would not appreciate the higher interest rates they would be charged on heavy machinery purchases. The same dilemma would confront policy makers if they were to contemplate manipulating the exchange value of the euro toward some macroeconomic performance objective or to correct for current account trade imbalances. If supply shocks affect different countries in the region to different degrees, the problem of cyclical divergence becomes even more acute.

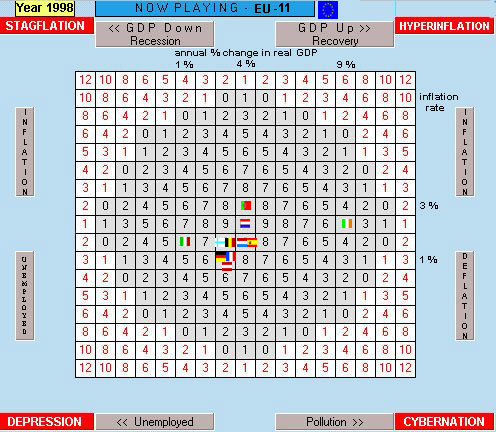

The fact is, however, that the E-11 countries have experienced remarkable cyclical convergence in the 1990s. As the display below reveals, the German and French economies performed like twiddle-dee and twiddle-dum in 1998. Their growth and inflation rates (and unemployment, too) were virtually the same. Eight of the eleven countries performed within 1 % of each other's growth and inflation rates. Only Ireland moved away from the pack with an extraordinary 9 % growth rate.

In the above display the E-11 countries are clustered closer together in 1998 than they were in 1992. While luck may have had something to do with this, there's more than luck at work here. Much of the credit for cyclical convergence is attributed to the efforts at policy coordination and the effectiveness of the Exchange Rate Mechanism (ERM), which was the precursor to the new monetary union. Whatever the cause, the situation in 1998 was almost ideal for introducing the euro and a common currency in January 1999.

The future success of the euro and monetary union now hinges on fiscal coordination, structural reforms, and greater degrees of labor mobility. If the countries fly together more like geese than independently minded crows, the euro will enhance prosperity in the region as promised. In any event, there's no turning back now. Whatever problems the new system may encounter, the performance of the region would likely be much worse if countries were to revert to independent, beggar-thy-neighbor competitive monetary and currency manipulation.

Statistical Tables

|

|

Rate |

Rate |

Rate |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rate |

Rate |

|

Rate* |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Recommended Link: http://europa.eu.int/euro